The life sciences have historically been one of the most attractive categories for investment. For some investors, being able to support the development of life-saving compounds is sufficiently rewarding. For others, the promise of a high-value return from an IPO or from an acquisition has motivated investment. The investment landscape is evolving with new technologies and investment laws that promise to change who and how they will invest.

To follow is a review of the current state of life sciences investment, how it is evolving, an understanding of crowdfunding legislation (the JOBS Act), and how the future of life sciences investment may change from present practices.

What is Happening with Funding in the Life Sciences?

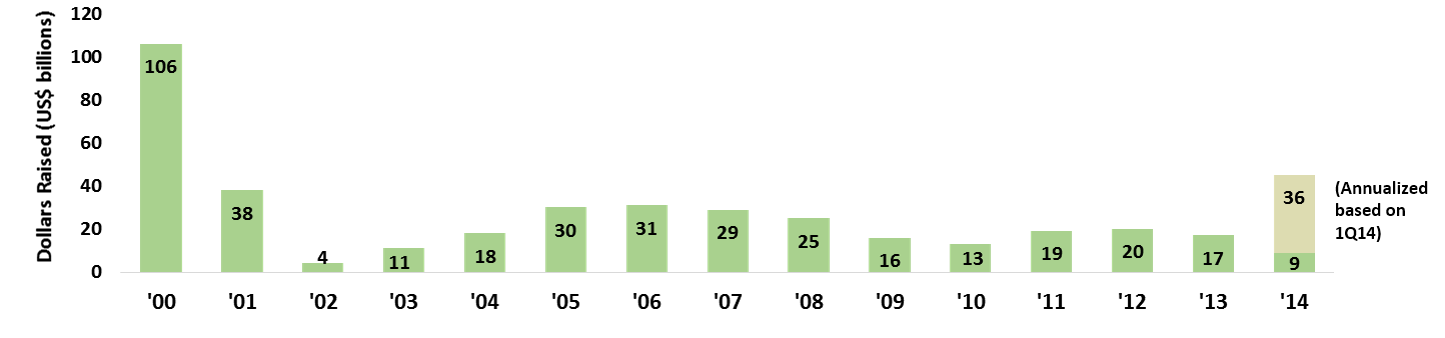

According to Fenwick and West's "Silicon Valley Venture Capital Survey First Quarter 2014", "a total of $8.9 billion was raised by 58 funds in 1Q14, a 82% increase in dollars from the $4.9 billion raised by 53 funds in 4Q '13 and a 9% increase in funds, according to Thomson/NVCA. 1Q '14 was the strongest quarter for fund-raising (in dollars) since 4Q '07 and saw the largest number of new venture funds (25) since 4Q '00." 1

Figure 1. U.S. Venture Capital Fundraising, Q1 '14

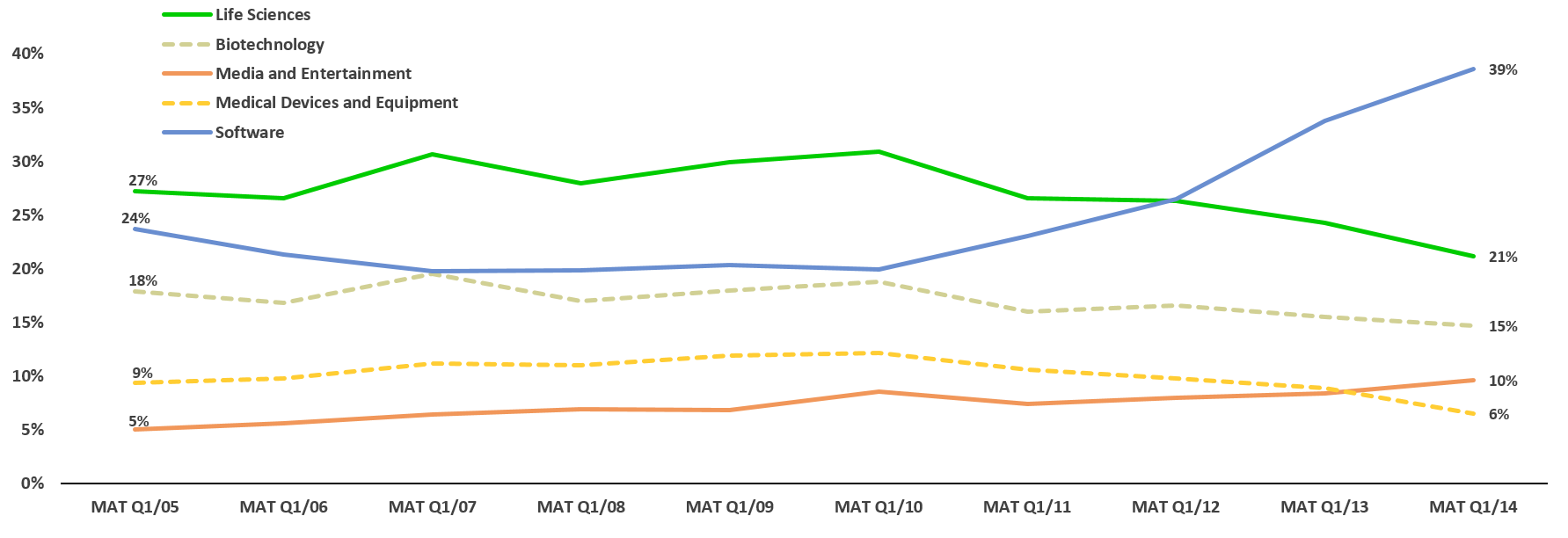

The life sciences' share of MAT Q1 '14 total venture capital investments is 21%; the lowest proportion since 2001 (Figure 2). It may be assumed that is an indication of a reduced interest for the life sciences category in favor of the Software category. [N.B. for the sake of clarity, those categories with less than 10% share for the years plotted were not shown]. 2

Figure 2. Select Categories' Share of Total VC Funding, MAT Q1 '14

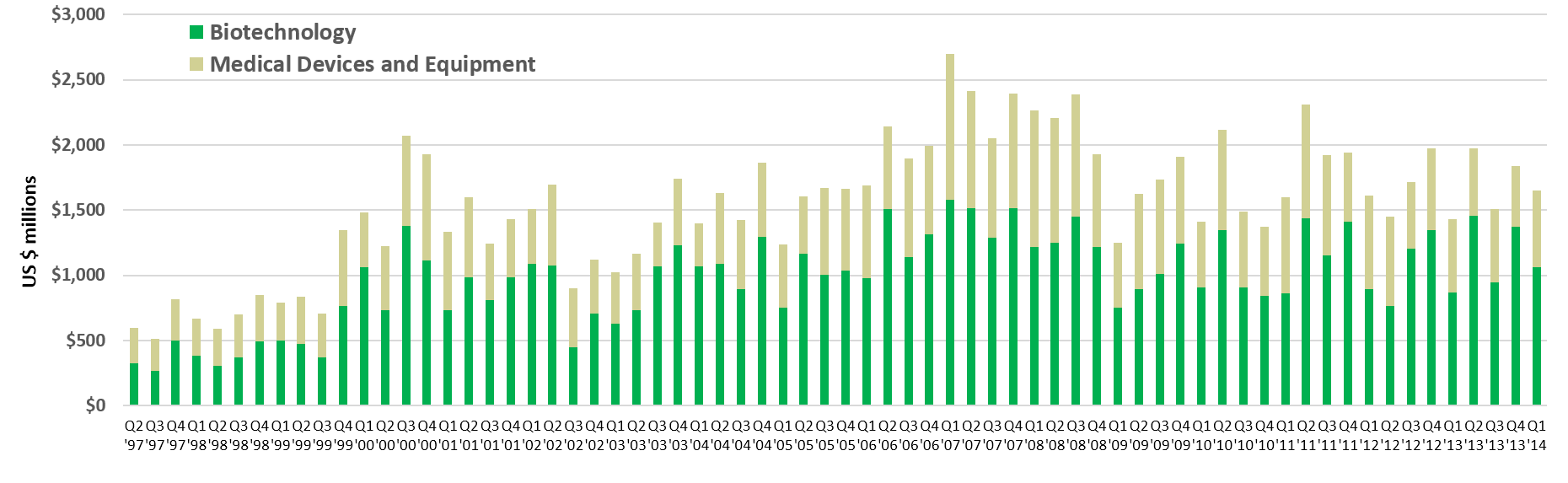

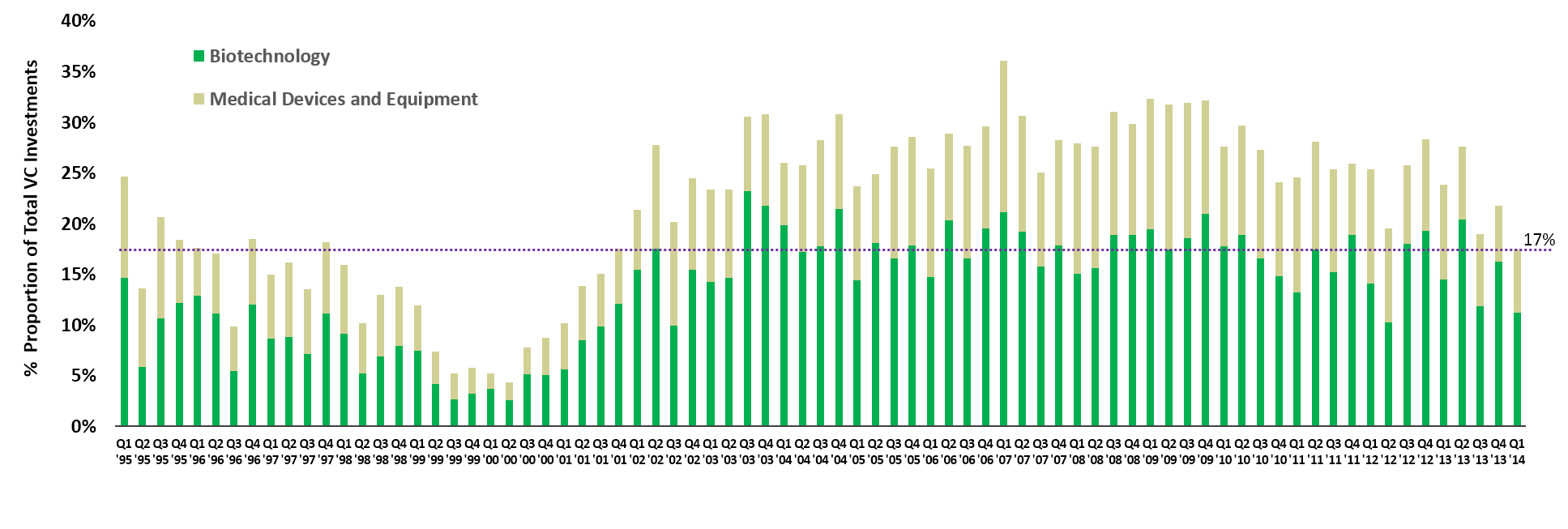

Quarter 1, 2014 data for venture capital funding for the life sciences shows $1.7 billion was invested in 173 deals (Figure 3). This compares favorably to Q1 '13 with $1.4 billion invested in 173 deals. (N.B. Life sciences is composed of the "Biotechnology" and "Medical Devices and Equipment" categories as per data source: PricewaterhouseCoopers' MoneyTreeTM Report). 3

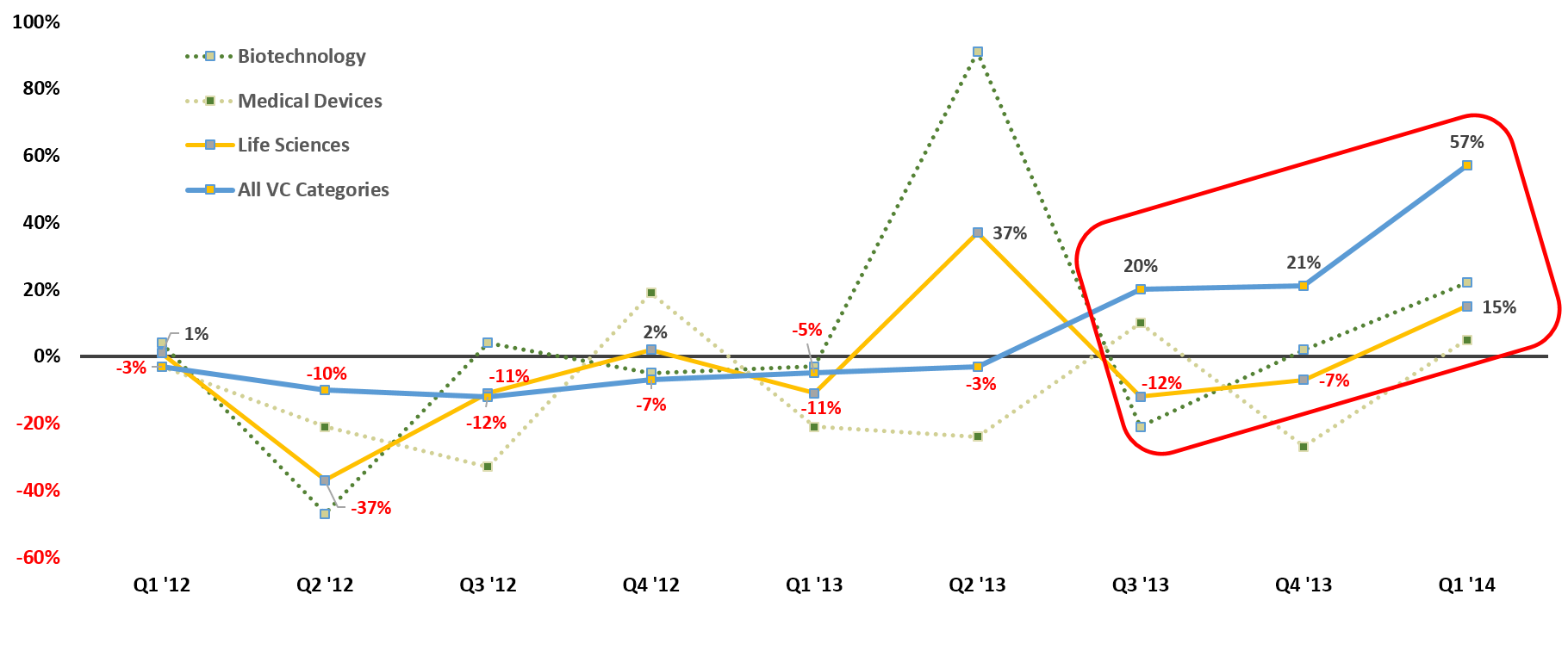

Figure 4 illustrates year-on-year percent change in deal value. Life sciences' venture capital investments increased by 15% during the first quarter of 2014, compared with the first quarter of 2013. In contrast, total venture funding jumped by 57%. This is the third consecutive quarter that the growth in total venture capital investment has significantly outperformed those of the life sciences' investments. A upward trend for the life sciences category is the positive inflection over time.

The life sciences' share of total venture capital investments was 17% for Q1 '14; the lowest proportion for a quarter since 2001.

Figure 5. Life Sciences As Percentage Share of Total VC Funding, Q1 '14

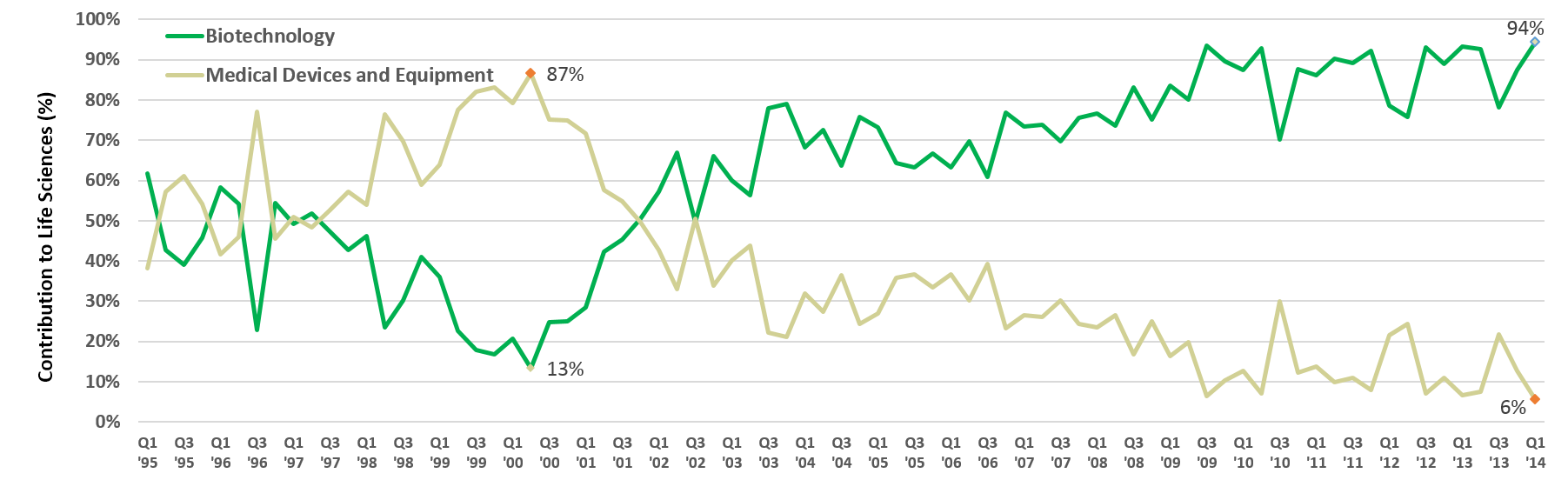

The Life Sciences category is composed of "Medical Devices and Equipment" and "Biotechnology". Figure 6 illustrates the continuing loss of appeal of the Medical Devices and Equipment category for funding (or, is it the overwhelming relative attractiveness of Biotechnology?), as it has fallen from 87% of Life Sciences' funding in 2000 to only 6% in 2014; truly a dramatic fall from grace!

Figure 6. Proportion of Life Sciences' Funding by Category, Q1 '14

Challenges Seeking Venture Capital Funding

In a report on the state of life sciences' funding, Jonathan Norris, Managing Director, Silicon National Bank, speaking at the December 2013 "Acceleration2013 [sic] Nutter Early Stage Life Sciences" conference, outlined some of the current industry challenges for early-stage companies seeking venture capital:

"Decreases in fund sizes and total dollars raised

Consolidation of the raw number of venture investors looking for life science deals

Reduction in overall venture investing into new companies, particularly in medical devices

The "exit bottleneck" overhang of 1,600 still private companies representing $38 billion in venture funds invested from 2000-2011.

Increasing presence of corporate investors into biotech companies, even as they continue to shy away from medical device investments." 3

Angel Investing in Life Sciences

While VCs avoid investment in early stage life science companies, angel investors frequently step in to fill the void: 4

In 2013, accredited angel investors put $24.8 billion into nearly 70,730 early-stage companies [all industry sectors].

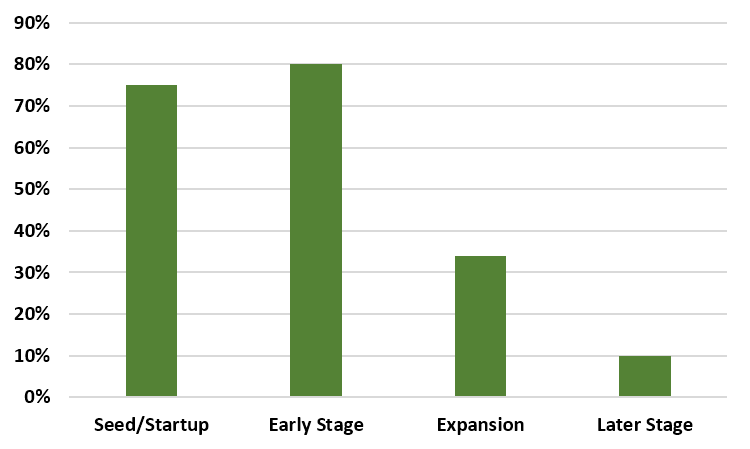

45% of 2013 angel investments were in the seed and start-up stages, up from 35% in 2012

The average angel deal size in 2013 was $350,830; an increase of 2.6% from 2012

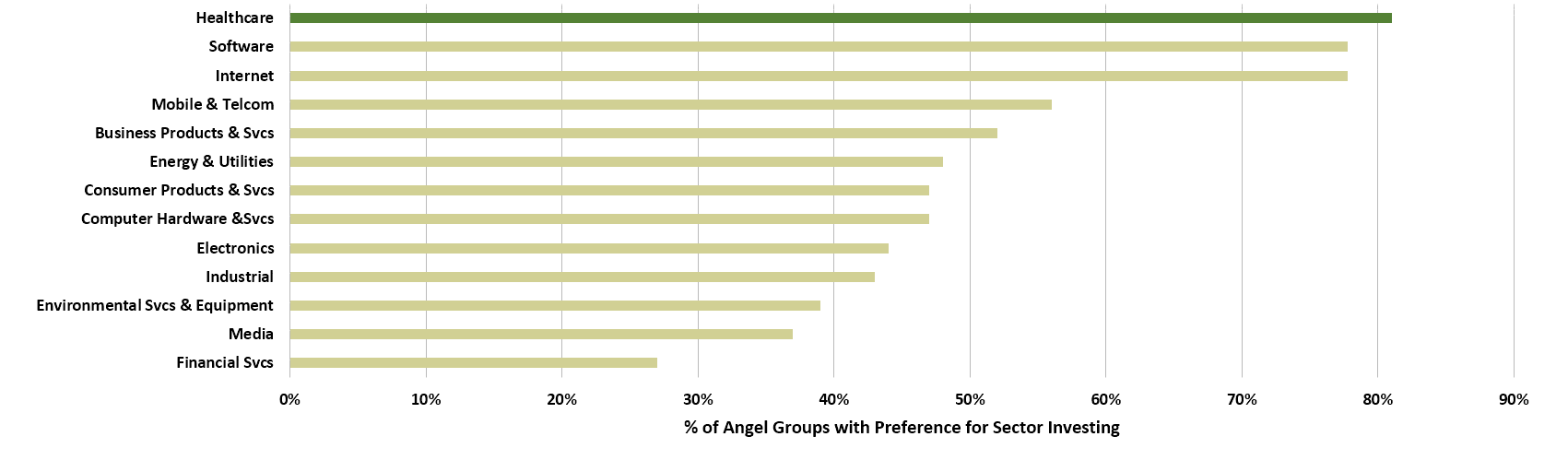

The Angel Capital Association's 2012 ACA Summit Confidence Survey revealed a high preference for investment in Healthcare as seen in Figure 7. 5

Figure 7. Sector Investing Preference of Angel Investors in 2012

In addition, The ACA highlights that accredited angel investors provide 90 percent of outside equity capital to startups, on top of mentoring and often additional expansion capital. The 2011 ACA Angel Group Confidence Survey indicated that the majority of angel groups preferred to invest in seed and early stage companies, not later stage.

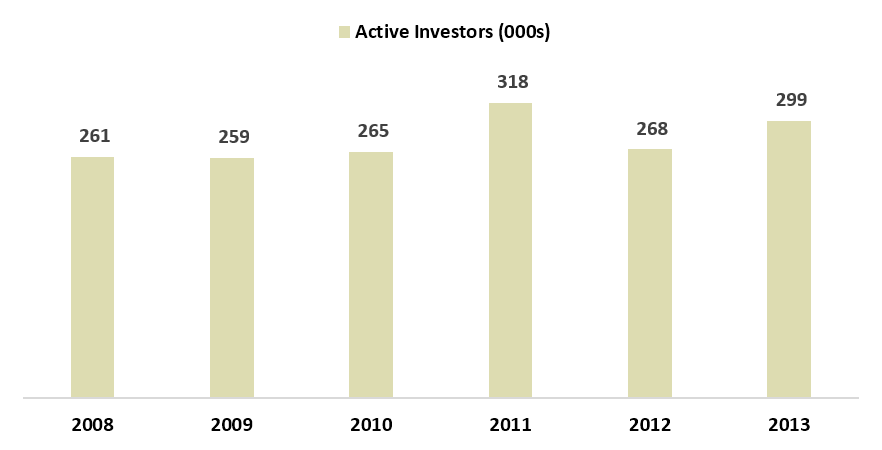

There were 298,800 active angel investors in 2013, a 11.4% increase over 2012. The number of active investors over the last six years are consistently above a quarter million.(Figure 9). 4

Figure 9. Number of Active Angel Investors, 2008 – 2013 (000s)

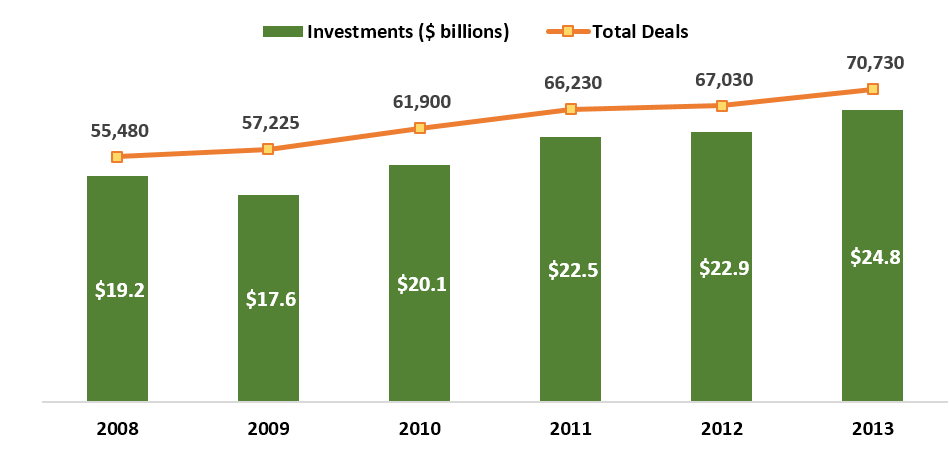

Angel investing in 2013 totalled $24.8 billion, an increase of 8.3% over 2012. The total number of investments (70,730) was 5.5% higher than 2012 levels.4

Figure 10. Angel Investing and Number of Deals, 2008 – 2013

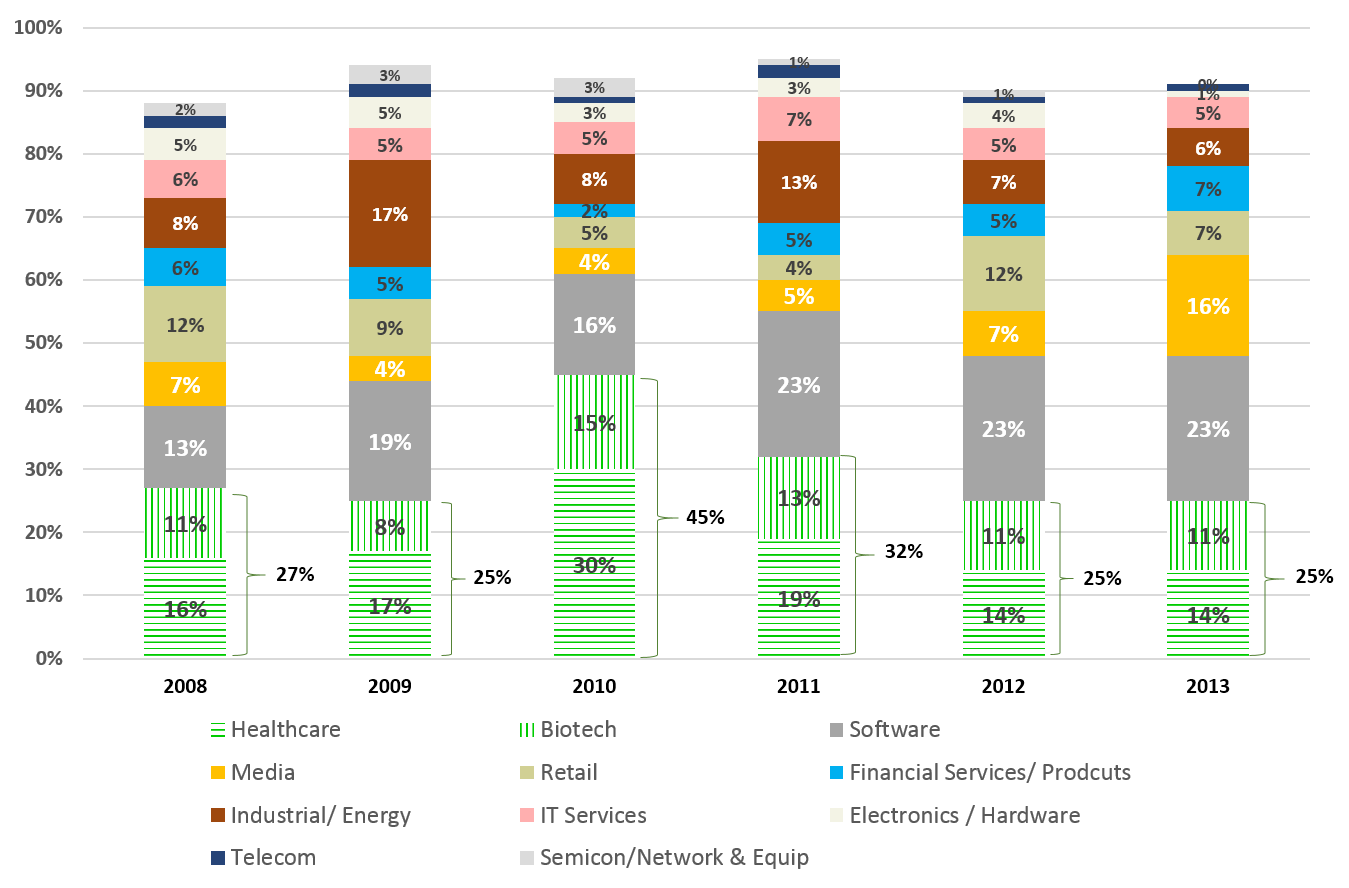

The share of Angel deals that were invested in the Life Sciences (Biotechology and Healthcare) was 25% for both 2013 and 2012. This is the second consecutive year without segment share growth for the Life Sciences; a likely result of the appeal of Software and Media opportunities for smart phones and internet applications. 4

Figure 11. Angel Investing by Sector, 2008 – 2013

Definitions

Biotechnology: Developers of technology promoting drug development, disease treatment, and a deeper understanding of living organisms. Includes human, animal, and industrial biotechnology products and services. Also included are biosensors, biotechnology equipment, and pharmaceuticals.

Healthcare Services/Medical Devices and Equipment: Includes both in-patient and out-patient facilities as well as health insurers. Included are hospitals, clinics, nursing facilities, managed care organizations, Physician Practice Management Companies, child care and emergency care. Manufactures and/or sells medical instruments and devices including medical diagnostic equipment (X-ray, CAT scan, MRI), medical therapeutic devices (drug delivery, surgical instruments, pacemakers, artificial organs), and other health related products such as medical monitoring equipment, handicap aids, reading glasses and contact lenses.

A current trend in angel investing involves syndicating wherein various angel investor groups collaborate on funding and are able to raise significant funding levels. For many companies, this level of investment allows companies to become revenue producing without ever needing VC involvement.

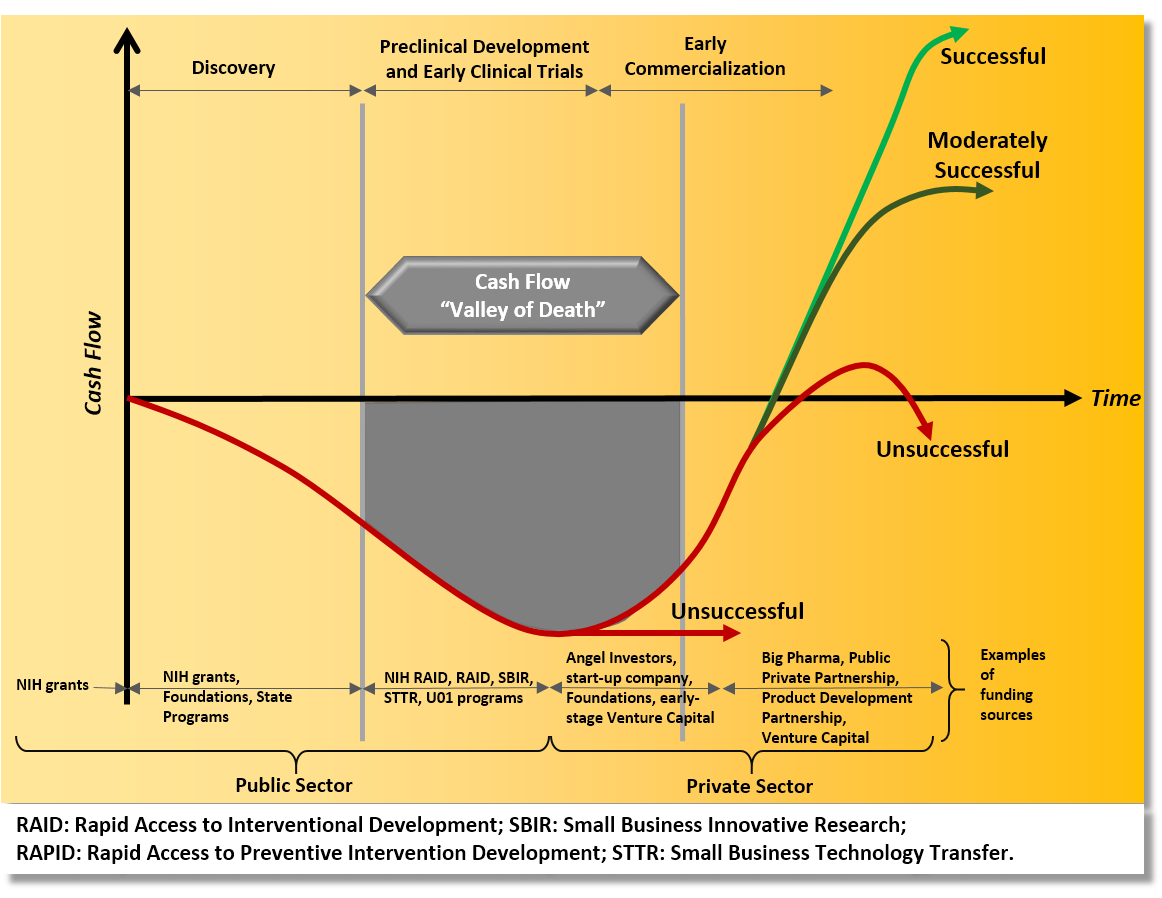

The Valley of Death

The Valley of Death (VoD) has been described as "the critical time between early- and late-stage development of new therapeutics, diagnostics, or devices. It is during this time when funding sources can dry up and technologies or interventions with tremendous potential can end up as casualties of an unpredictable and often unforgiving business environment."17 "In the valley of death, additional financing is usually scarce, leaving the firm vulnerable to cash flow requirements. Traversing it requires an intelligent blend of public and private sector investment."7

Figure 12 illustrates the VoD concept for a pharmaceutical product in development. 8 Other product categories and industries have similar kinds of development, funding components, and associated timings.

Figure 12. The Valley of Death in Pharmaceutical Funding

Causes of the Valley of Death

The main causes of the VoD are:

Long development time

High failure rate

Risk/Return on investment relative to other investor opportunities

A brief overview of each of these factors follows.

Long Drug Development Time

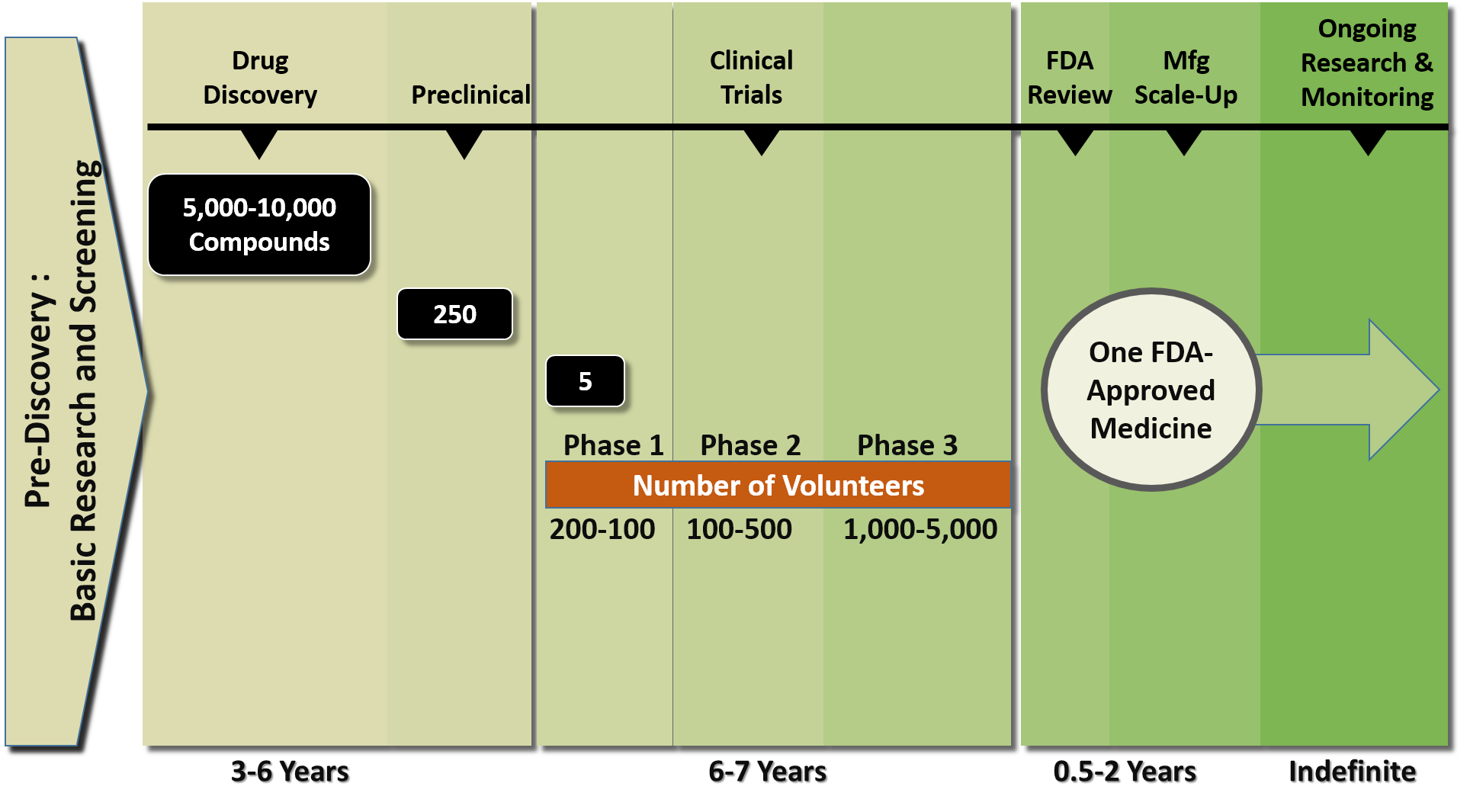

The average time needed for drug development ranges from 10 to 15 years8 when measured from target identification through approval. In addition to delaying the availability of a new therapy for patients, the long development time increases the overall cost, delays the time to a return on the investment, and reduces the period of sales protected from generics (which impacts the economics for innovators, investors, and the health care system in differing ways).

Figure 13 illustrates the approximate time needed, work performed, and phase of development for a typical medicine's development and approval as provided in "2013 Biopharmaceutical Research Industry Profile", published by the Pharmaceutical Research and Manufacturers of America's (PhRMA). What is obvious from the chart is the high level of attrition seen in the number of compounds in play from Discovery through the Clinical phases. This process has much to do with increasing both the time required and the chance of failure as will be described below.

Figure 13. The Research and Development Process

High Failure Rates

In addition to long development times, the biopharma industry has to endure high failure rates for products in development. This increases the overall cost, delays the time to return on investment, and reduces investor confidence and category attractiveness.

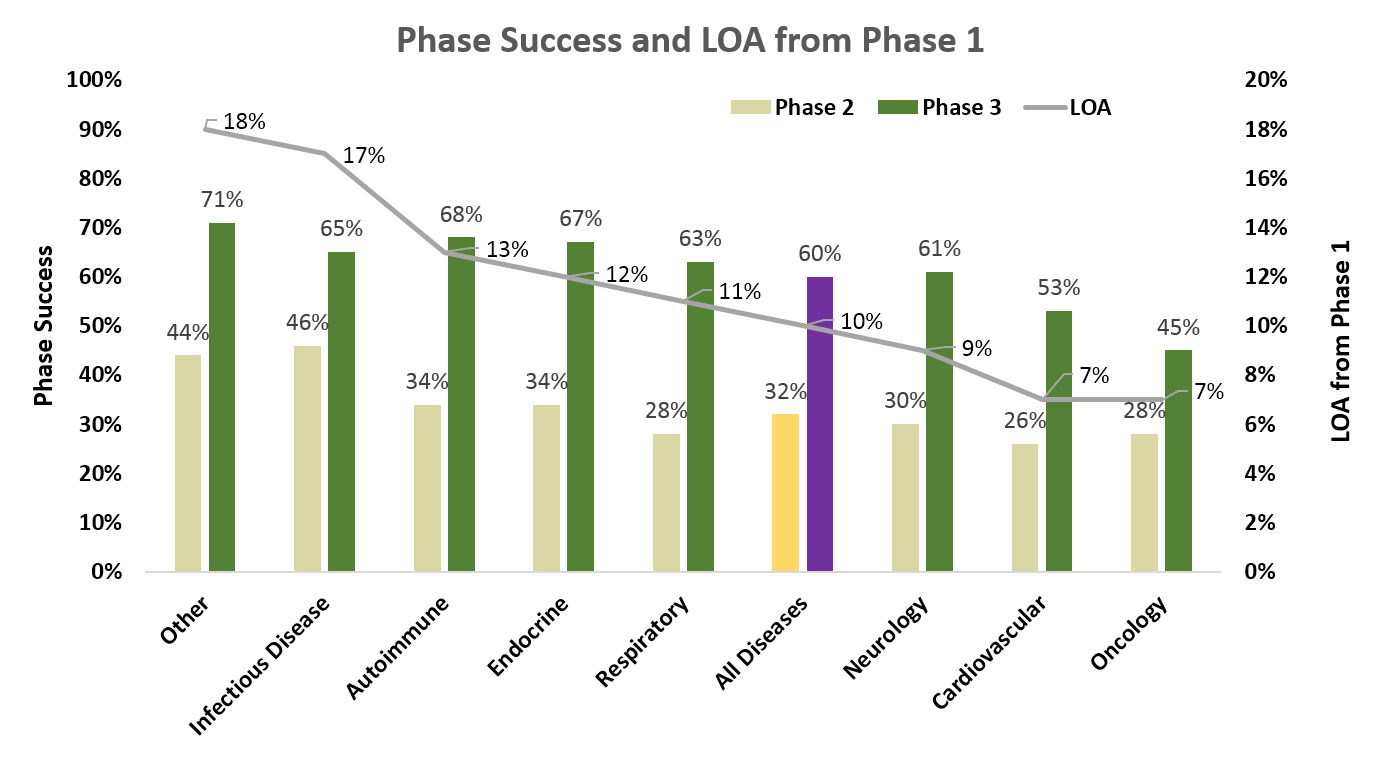

In "Clinical development success rates for investigational drugs" by Hay et al, Nature Biotechnology January 2014, the authors reviewed clinical development success rates across the industry and described their work as "...the largest and most recent of its kind, examining success rates of 835 drug developers, including biotech companies as well as specialty and large pharmaceutical firms from 2003 to 2011." 10

Figure 14 summarizes the phase success and likelihood of approval (LOA) from phase 1 by disease data for all indications. The bars represent phase 2 and phase 3 success rates and the line represents LOA from Phase I. The LOA ranges from 28% to 46% for compounds in Phase II and indicates the high level of difficulty historically experienced in drug development. How to improve this process to improve the LOA is the subject of much discussion and debate and will not be resolved soon.

Figure 14. Likelihood of Success by Development Phase

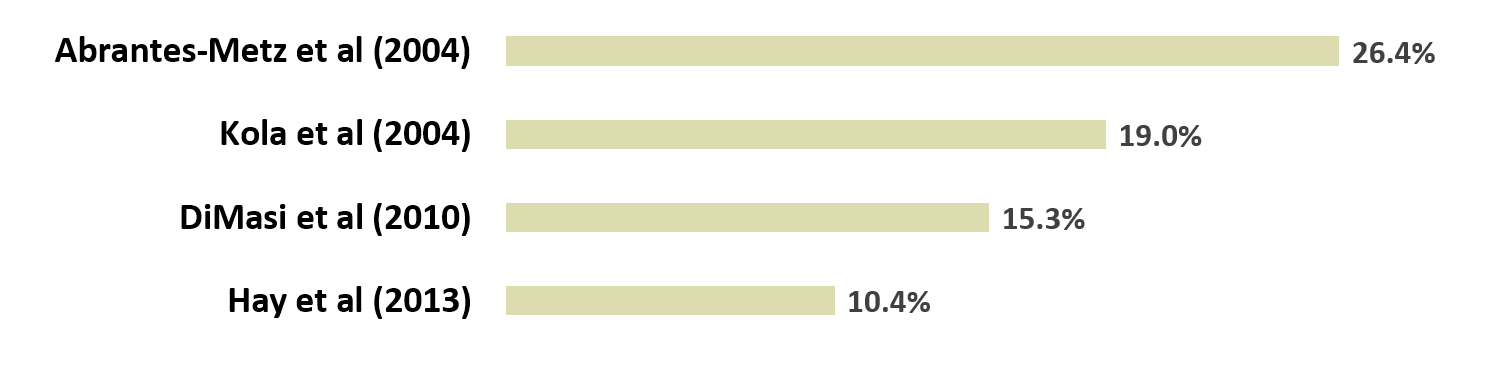

Potentially more troubling is one of the conclusions reached by Hay et al: "The data presented in this study suggest industry-wide productivity may have declined from previous estimates." (Figure 15) This conclusion is based on their comparison of their study data versus that of earlier, similar studies from 2004 and 2010 as reported by their authors. The data reported in Hay et al indicates a worsening of the LOA over time: by approximately 60% since 2004 and by 32% since 2010 [emphasis added].

Figure 15. Reported Likelihood of Approval Rates by Study Report

Risk/Return on Investment

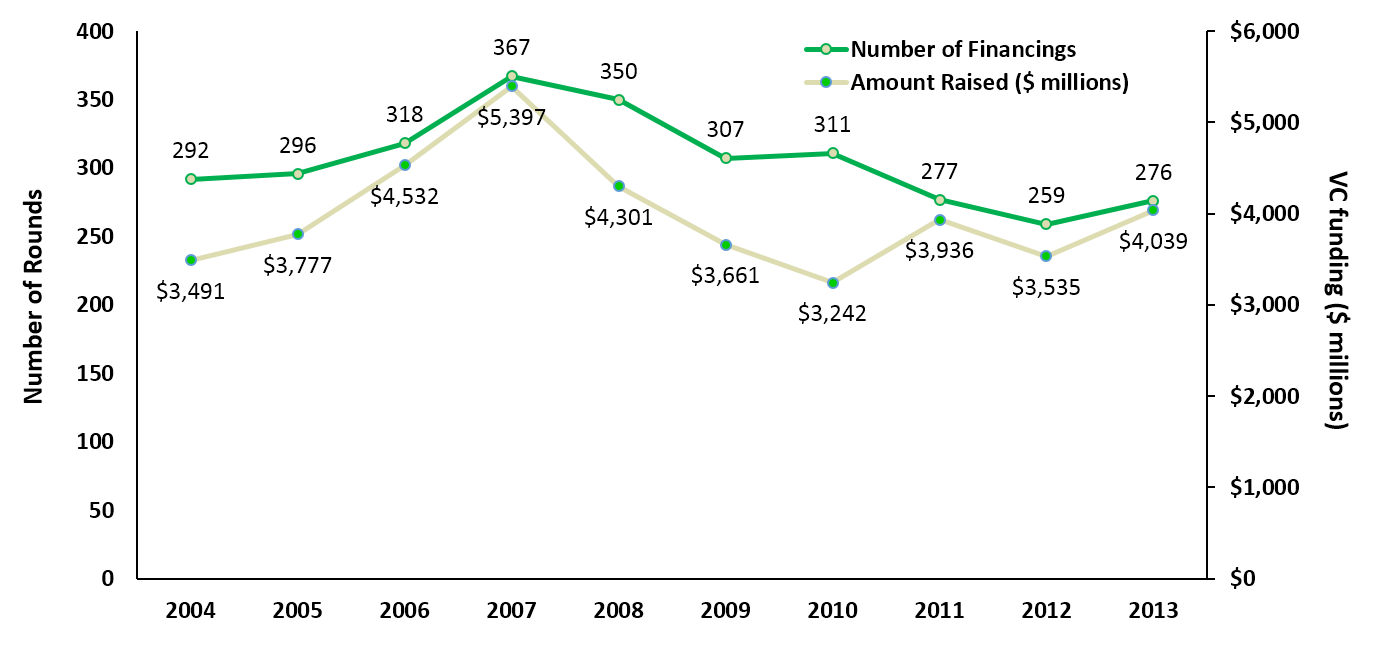

In 2013, there was a slight up-tick in the amount and number of financings for biotech (Figure 16) compared to 2012, as reported in Nature Biotechnology, May 2014. 11 Though this is positive when compared to 2012, the number and value of the deals are still much lower than those seen in 2006-2008.

Figure 16. Amount of Venture Capital Raised

The number of venture capital firms decreased in 2013 (Figure 17). Brady Huggett, Business Editor, Nature, who authored the report stated: "It should be noted that these funds are investing in innovative private biotech companies at all stages of development; very few funds remain active in the earliest stages to support startup creation [emphasis added]." 11

Figure 17. Number of Active Venture Capital Firms

As in past years, only about 2% of VC money went to start-ups; the remainder went to companies with profiles matching product development, generating revenue, and/or being profitable (Table 1). Though "...very early-stage start-ups require less money than private companies undertaking the later, more expensive stages of product development"8, these data also point to the preference of VCs to invest in lower-risk opportunities, i.e., anything but start-ups.

Table 1. VC Investment by Stage of Development

2009

2010

2011

2012

2013

Startup total

$58

$17

$52

$51

$80

Product development

$2,985

$2,528

$3,476

$2,896

$3,412

Generating revenue

$550

$671

$386

$575

$540

Profitable

$68

$27

$22

$14

$6

Total

$3,661

$3,242

$3,936

$3,536

$4,039

No love for early stage...

"...at the earliest stages of the private biotech company pipeline, the pool of VC funding for startups continues to stagnate, and the number of venture funds focusing on early stage is dwindling..."

Brady Huggett, Business Editor, "Nature Biotechnology"

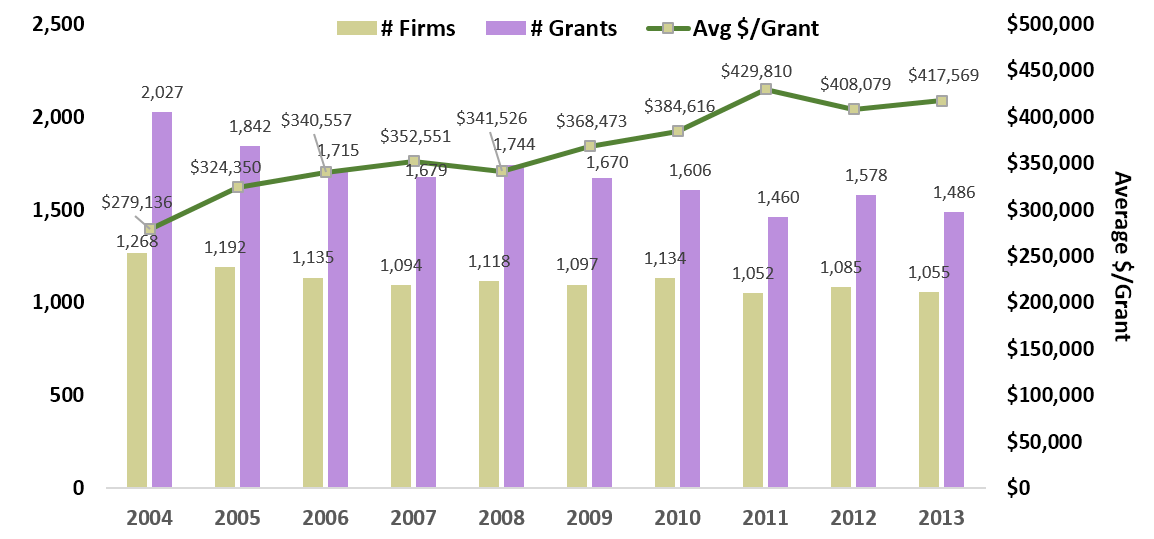

For the U.S., there has not been an increase in the number of SBIR or STTR grants to pick up the funding slack (Figure 18). Both the number of firms receiving grants and number of grants provided have been essentially decreasing since 2004. The grants have increased in size relative to inflation: $280,000 in 2003 is worth $350,000 inflation adjusted to 2014, compared with the $418,000 average value awarded in 2013 (a 19% inflation-adjusted increase). Though the amount awarded may be higher, there is more competition for fewer awards; again indicating the increasing difficulty for securing early-stage funding. 7

Figure 18. SBIR & STTR Grant Metrics

VCs Abandoning the Funding of Life Sciences

In "The View Beyond Venture Capital", Nature Biotechnology, January 2014, Ford and Nelson lay out why they believe access to funding has become more challenging, especially for startups. They suggest the following as the main reason for the pull-back in funding for early-stage life science companies: 12

"The main reason for the withdrawal (especially from VCs in the early-stage life science space) was generally meager returns across the asset class; despite the high risk and long lock-up periods that investors accepted in return for a promise of premium performance, VCs were often not returning any more capital than investors would have earned by making more liquid investments in the public small caps market. Returns from venture capital funds have not outperformed the public markets since the late 1990s."

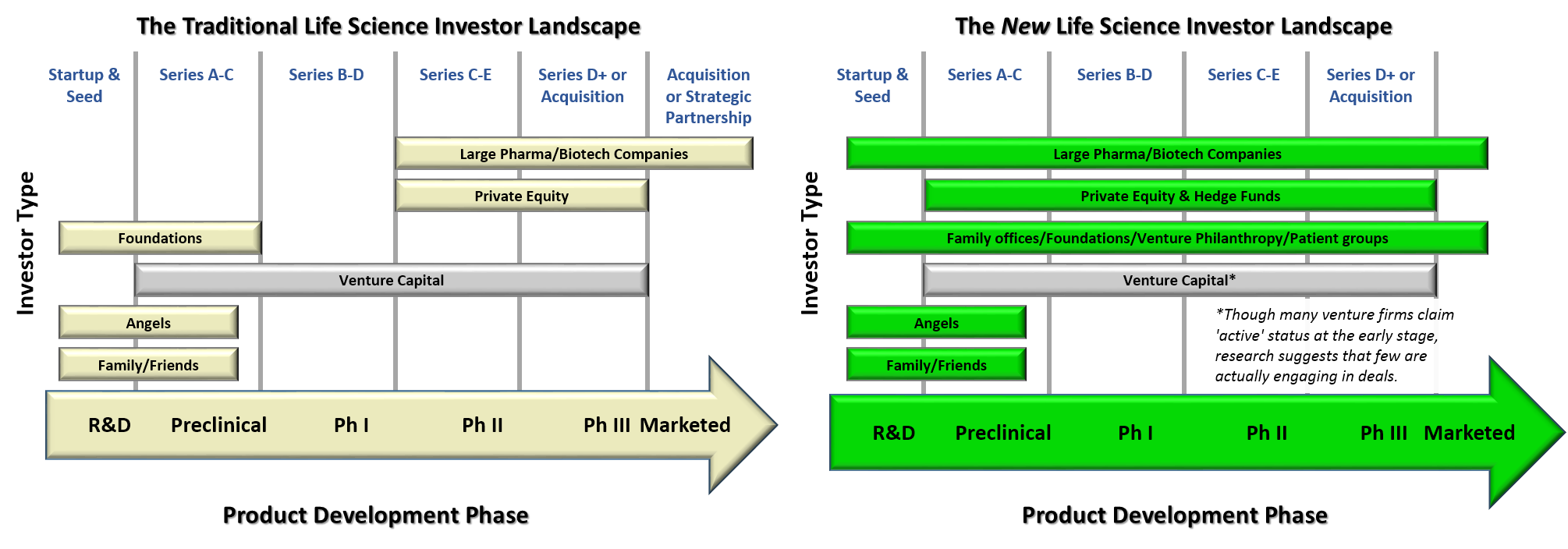

The changes in investing patterns have altered the life science investor landscape. Ford and Nelson provided the following schema that illustrates their view on these changes. (Figure 19) 12

Figure 19. Evolution of Life Science Investor Landscape

Missing from their New Life Science Investor Landscape are the accredited investors enabled via Title II of the JOBS Act and crowdfunding participants via Title III (once TItle III is finalized and approved by the U.S. SEC).

This all leads to the next logical questions: What is crowdfunding and what are the differences between Title II and Title III investors and investing?

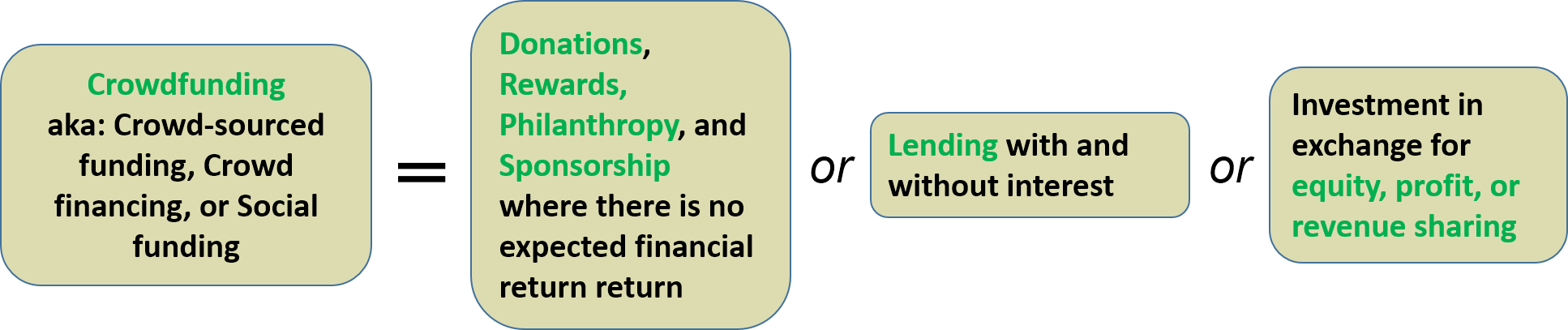

What is Crowdfunding?

In its simplest form, crowdfunding (sometimes called crowd-sourced funding, crowd financing, or social funding) is asking a group of people to fund a new venture.

Crowdfunding Definition

"An Internet-enabled way for businesses or other organizations to raise money in the form of either donations or investments from multiple individuals."

"Crowdfunding's Potential for the Developing World". 2013.13

Investopedia defines crowdfunding as: "The use of small amounts of capital from a large number of individuals to finance a new business venture. Crowdfunding makes use of the easy accessibility of vast networks of friends, family and colleagues through social media websites like Facebook, Twitter, and LinkedIn to get the word out about a new business and attract investors. Crowdfunding has the potential to increase entrepreneurship by expanding the pool of investors from whom funds can be raised beyond the traditional circle of owners, relatives and venture capitalists." 14

Why the Excitement Now with Crowdfunding?

The big deal is that until passage and enactment of the JOBS Act, crowdfunding (and the internet) could not be used to offer or sell securities to the general public. "The Act eliminates the prohibition against general solicitation or general advertising in any offering of securities pursuant to Rule 506 under the Securities Act for all purposes of the 'federal securities laws,' provided certain conditions are met." 15,16

"Crowdfunding itself is not new. Websites like Kickstarter and Indiegogo help all sorts of businesses, organizations and people raise money through small individual contributions for an identifiable idea or business. Issuers and intermediaries relying on Regulation Crowdfunding expect to further democratize investing in start-ups, because any investor, whether or not accredited, may invest in these securities." [Note: nonaccredited investor investing is covered by Title III, not yet in effect.] 18

Crowdfunding is only possible and legal in the United States by the lawful processes described in Title II and Title III of the Jumpstart Our Business Startups Act (JOBS Act) [discussed below], signed into law by President Obama on 5 April 2012, and as regulated by the US Securities and Exchange Commission (SEC).

At present, only Title II (for accredited investors only) of the JOBS Act has been enacted; equity crowdfunding under Title III [for unaccredited (aka most people) investors] has not been approved as the SEC continues to solicit and assess comments from interested parties.

Title II approval means that companies can now publicly advertise on web portals on the internet that they are looking for funding. Title II also allows for nonaccredited investors to invest money in new opportunities (within certain limits and under discrete conditions). Likewise, under Title III, accredited investors can now seek out opportunities (now able to be freely advertised/solicited) they wish to fund on their own, without having to be a friend or family or part of a sophisticated investment group or organization.

What remains to be seen is whether the Title III portion of the JOBS Act will ever gain final approval and enactment by the SEC and if it does, how significant it will be as a source of financing for life sciences companies. Given the presumed regulatory burdens that will be in place for funding portals, the limits on the amount of a donation by individuals, and the typically large sums needed by life sciences companies, Title III funding may prove to be of little significance. There is a much higher likelihood that Title II portals will prove to be significant sources of funding.

What Kinds of Crowdfunding Are There?

The JOBS Act subtitled Title III of the legislation as crowdfunding. However, colloquially the term is used rather interchangeably for funding via an internet portal whether it is in accordance with Title II or will follow Title III when it is in effect. So, a word of caution: make sure that you understand which crowdfunding type you may be discussing with someone as they may be using a different definition.

Figure 20: Basic Types of Crowdfunding

Most sources indicate that there are two basic types of crowdfunding; each with their own subtypes: 15,16,17

Donation

Donation or Charity: Contributions go towards a charitable cause without any expectation of a return on your investment. (Your money provides for 50 children in Country X to receive a book.). Example sites include GoFundMe, Rally, and Global Giving.

Rewards:"...where contributions are exchanged for current or future of goods or services. Individuals or companies who launch campaigns may compensate contributors with something like a t-shirt, a copy of whatever they're building or even just a thank you. Rewards-based crowdfunding is perhaps the most prolific form of crowdfunding currently taking place in the US. Examples include: Kickstarter [it's not for businesses, causes, charities, or personal financing needs] and Indiegogo [approves donation-based fund-raising campaigns for most anything - music, hobbyists, personal finance needs, charities and whatever else you could think of (except investment)]represent this form." 18,19

Investment

Equity: Investors receive a stake in the company. (If Newco goes big, you get a percentage of the prize). Examples of these include Crowdfunder, CircleUp, and MicroVentures. Only accredited investors can participate (remember, Title II has been approved but no Title III approval yet).

Lending: Investors are repaid for their investment over a period of time sometimes with interest and sometimes without. (You invest in Newco and get your money paid back over time). Examples of crowdfunding platforms that use the peer-to-peer lending model include Kiva, LendingClub, and Prosper.

What is the Crowdfunding Market Size?

Some reported estimates of the current value of crowdfunding:

According to Massolution: "Crowdfunding platforms raised $2.7 billion and successfully funded more than 1 million campaigns in 2012." Massolution forecasted an 88% increase in global crowdfunding volumes in 2013, to $5.1 billion. 23

UC Berkeley College of Engineering: "From the lenses of Angels, VCs and Small Business lending, we believe a market as large as $3.98B per year could rapidly evolve." 24

"The SEC estimates that at least 8.7 million U.S. households, or 7.4% of all U.S. households, qualified as accredited investors in 2010, based on the net worth standard in the definition of "accredited investor." 20

Wefunder.com reports "Only 3% or 256,000 of the 8 million accredited investors in the US are active angels, and those angels invest $21 billion each year." 26

The Angel Capital Association states, "The best available estimates are that over 300,000 people have made an angel investment in the last two years (including accredited and non-accredited investors) [N.B. There is no date associated with the report or the data it mentions.]. Many more people could become angels - based on a net worth of $1 million or more, the potential number of angel investors is 8 million." 21

Assuming that 3% of the eight million accredited investors invest $21 billion, would it be possible that the balance of these investors (the 97% on the sidelines) then be able to invest $700 billion? If current investment participation just doubles from 3% to 6%, then another $21 billion might be put into investments. Might greater acceptance and awareness of accredited crowdfunding facilitate this level of investing?

What is the JOBS Act?

On April 5, 2012, President Obama signed the JOBS Act (Jumpstart Our Business Startups Act) into law to encourage funding of small businesses by reducing securities regulations and by helping them get access to capital in new ways. 24,25

The JOBS Act has numerous elements but the main ones have been well described in a May 2014 summary, "The JOBS Act at Two", from Morrison/Foerster: 29

Title I, Reopening American Capital Markets to Emerging Growth Companies: Most commonly referred to as the "IPO On-Ramp", this Title is meant to encourage smaller companies to go public through a process where public company obligations would be phased-in over time.

Title II, Access to Capital for Job Creators: This Title removes the prohibition against general solicitation and general advertising in private offerings under Regulation D, provided that all of the purchasers of securities are accredited investors. The Title also addresses certain broker-dealer issues for these offerings.

Title III, Crowdfunding: This Title provides an exemption for "crowdfunding," by permitting offerings up to $1 million. Requirements targeted at investor protection are imposed on the issuer and the intermediary involved in the crowdfunding effort. The Title also addresses certain broker-dealer issues for these offerings.

Title IV, Small Company Formation: This Title is what is commonly referred to as "Regulation A" reform, and it creates a new exemption for offerings up to $50 million.

Title V, Private Company Flexibility and Growth: This Title increases the Exchange Act registration stockholder of record threshold from 500 to 2,000 (only 500 of which can be non-accredited investors).

Title VI, Capital Expansion: This Title increases the stockholder of record threshold from 500 to 2,000 for banks and bank holding companies, and provides that a bank or bank holding company could terminate 1934 Act registration if the number of holders of record drops to less than 1,200.

"The Jumpstart our Business Startups Act ("JOBS Act") was a bipartisan effort to create jobs by making it easier for start-up companies to deal with securities laws when raising capital. The major provisions of the JOBS Act:

Create the "IPO On-Ramp," which provides regulatory relief for "Emerging Growth Companies"

Allow advertising of private offerings in which securities are sold only to "accredited investors"

Allow raising capital through "crowdfunding"

Create exemptions for "Small Offerings"

Change the number of record shareholders that triggers ongoing securities reporting requirements

The following panels were developed by reproducing content from the Morrison/Foerster document. They provide key comments and further details on each element of the first three parts of the JOBS Act; Title IV-VI will not be covered in this communication.

Permits filing a registration statement with the SEC on a confidential basis.

Expands the range of permissible pre-filing communications made to qualified institutional buyers, or QIBs, or institutional accredited investors.

EGCs may now engage in oral or written communications with QIBs and institutional accredited investors in order to gauge their interest in a proposed IPO (i.e. "test-the-waters") either prior to or following the first filing of the IPO registration statement.

Requires EGCs to provide only two years of audited financial statements to the SEC (rather than three years), and delays the auditor attestation on internal controls requirement.

Exempts EGCs from:

The mandatory say-on-pay vote requirement;

The Dodd-Frank Act-required CEO pay ratio rules, and permits the use of certain smaller reporting company scaled disclosure;

Any new or revised financial accounting standard until the date that such accounting standard becomes broadly applicable to private companies; and

Any rules requiring mandatory audit firm rotation or a supplement to the auditor's report that would provide additional information regarding the audit of the company's financial statements (no such requirements currently exist).

Emerging Growth Company Defined

An EGC is defined as an issuer with total annual gross revenue of less than $1 billion (with such threshold indexed to inflation every five years).

An EGC would retain that status until:

The last day of the fiscal year in which the issuer had $1 billion or more in annual revenues;

The last day of the fiscal year following the fifth anniversary of the issuer's IPO;

The date on which the issuer has, during the previous rolling 3-year period, issued more than $1 billion in non-convertible debt:

Debt issued in a public or an exempt offering (not outstanding);

Rolling three-year period from the time the issuer establishes its EGC status; or

The date when the issuer is deemed to be a "large accelerated filer" (as defined by the SEC).

Table of changes in disclosure requirements.

Disclosure Requirements

Prior to JOBS Act

Under the JOBS Act

Financial Information in SEC Filings

3 years of audited financial statements

2 years of audited financial statements for smaller reporting companies

Selected financial data for each of 5 years (or for life of issuer, if shorter) and any interim period included in the financial statements

2 years of audited financial statements

Not required to present selected financial data for any period prior to the earliest audited period presented in connection with an IPO

Within 1 year of IPO, EGC would report 3 years of audited financial statements

Communications Before and During The Offering Process

Limited ability to "test-the-waters"

EGCs, either prior to or after filing a registration statement, may "test-the-waters" by engaging in oral or written communications with QIBs and institutional accredited investors to determine interest in an offering

Auditor Attestation on Internal Controls

Auditor attestation on effectiveness of internal controls over financial reporting required in second annual report after IPO

Non-accelerated filers not required to comply

Transition period for compliance of up to 5 years

Accounting Standards

Must comply with applicable new or revised financial accounting standards

Not required to comply with any new or revised financial accounting standard until such standard applies to companies that are not subject to Exchange Act public company reporting

EGCs may choose to comply with non-EGC accounting standards but may not selectively comply

Executive Compensation Disclosure

Must comply with executive compensation disclosure requirements, unless a smaller reporting company (which is subject to reduced disclosure requirements)

Upon adoption of SEC rules under Dodd-Frank, will be required to calculate and disclose the median compensation of all employees compared to the CEO

May comply with executive compensation disclosure requirements by complying with the reduced disclosure requirements generally available to smaller reporting companies

Exempt from requirement to calculate and disclose the median compensation of all employees compared to the CEO

FPIs entitled to rely on other executive compensation disclosure requirements

Say-on-Pay

Must hold non-binding advisory stockholder votes on executive compensation arrangements

Exempt from requirement to hold non-binding advisory stockholder votes on executive compensation arrangements for 1 to 3 years after no longer an EGC

The SEC adopted a new paragraph (c) in Rule 506, which permits the use of general solicitation, subject to the following conditions:

The issuer must take reasonable steps to verify that the purchasers of the securities are accredited investors;

All purchasers of securities must be accredited investors, either because they come within one of the enumerated categories of persons that qualify as accredited investors or the issuer reasonably believes that they qualify as accredited investors, at the time of the sale of the securities; and

The conditions of Rule 501 and Rules 502(a) and 502(d) are satisfied.

An issuer may still choose to conduct a private offering in reliance on Rule 506(b) without using general solicitation.

Reasonable Steps to Verify Investor Sales

The final rule retains the principles-based guidance, highlighting that the inquiry to be undertaken may differ depending on the facts and circumstances. The SEC provides a list of factors to consider:

The nature of the purchaser. The SEC describes the different types of accredited investors, including broker-dealers, investment companies or business development companies, employee benefit plans, and wealthy individuals and charities;

The nature and amount of information about the purchaser. Simply put, the SEC states that "the more information an issuer has indicating that a prospective purchaser is an accredited investor, the fewer steps it would have to take, and vice versa;" and

The nature of the offering. The nature of the offering may be relevant in determining the reasonableness of steps taken to verify status, i.e., issuers may be required to take additional verification steps to the extent that solicitations are made broadly, such as through a website accessible to the general public, or through the use of social media or email.

The final rule does not provide for a safe harbor; however, it does set out a supplemental non-exclusive list of methods that may be used to satisfy the verification requirement, including:

A review of IRS forms for the two most recent years and a written representation regarding the individual's expectation of attaining the necessary income level for the current year;

A review of bank statements, brokerage statements, tax assessments, etc. to assess assets, and a consumer report or credit report from at least one consumer reporting agency to assess liabilities;

A written confirmation from a registered broker-dealer, RIA, CPA, etc.; and

For existing investors (pre-506(c) effective date), a certification.

New "Bad Actor" Disqualification

"Bad actor" disqualification requirements prohibit issuers and others, such as underwriters, placement agents, directors, officers, and shareholders of the issuer, from participating in exempt securities offerings, if they have been convicted of, or are subject to court or administrative sanctions for, securities fraud or other violations of specified laws.

On July 10, 2013, the SEC issued its final rules regarding "bad actors" for Regulation D. The amendments became effective on September 23, 2013.

The SEC has released multiple CD&Is to provide further guidance.

Recent Developments

Relatively few offerings using general solicitation (compared to traditional Rule 506(b) offerings)

Investor verification

Perceived difficulties or cost associated with verification

SEC staff has emphasized principles-based approach and noted that it is unlikely that additional guidance will be forthcoming on verification

CFTC's failure to address the ability of certain funds to engage in general solicitation

"Chilling" effect associated with the SEC's proposed Reg D amendments

Ability to engage in "accredited investor" crowdfunding

Concerns regarding the types of communications that would be or may be deemed to constitute a "general solicitation"

The SEC Staff has referred to its prior no-action letter guidance regarding the types of communications that would not be deemed to constitute a general solicitation

Title III provides an exemption that could apply to crowdfunding offerings.

The SEC voted to release proposed rules on October 23, 2013, and the deadline for comments on the proposed rules expired on February 3, 2014.

The SEC's proposed rules track the statute closely.

The aggregate amount sold to all investors by the issuer should not be more than $1,000,000.

This includes any amount sold in reliance on the exemption during the 12-month period preceding the date of the transaction.

The aggregate amount sold to any investor by the issuer, including any amount sold in reliance on the exemption during the 12-month period preceding the date of the transaction, should not exceed:

The greater of $2,000 or 5 percent of the annual income or net worth of the investor, as applicable, if either the annual income or the net worth of the investor is less than $100,000; or

10 percent of the annual income or net worth of an investor, as applicable, not to exceed a maximum aggregate amount sold of $100,000, if either the annual income or net worth of the investor is equal to or more than $100,000.

The transaction must be conducted through a broker or "funding portal."

Information should be filed and provided to investors regarding the issuer and offering, including financial information based on the target amount offered.

The provision prohibits issuers from advertising the terms of the exempt offering, other than to provide notices directing investors to the funding portal or broker, and requires disclosure of amounts paid to compensate solicitors promoting the offering through the channels of the broker or funding portal.

Issuers relying on the exemption need to file with the SEC and provide to investors, no less than annually, reports of the results of operations and financial statements.

A purchaser in a crowdfunding offering can bring an action against an issuer for rescission in accordance with Section 12(b) and Section 13 of the Securities Act, as if liability were created under Section 12(a)(2) of the Securities Act, in the event that there are material misstatements or omissions in connection with the offering.

Securities sold on an exempt basis under this provision are not transferrable by the purchaser for a one-year period beginning on the date of purchase, except in certain limited circumstances.

The exemption is only be available for domestic issuers that are not reporting companies under the Exchange Act and that are not investment companies, or as the SEC otherwise determines is appropriate.

Bad actor disqualification provisions similar to those required under Regulation A would also be required for exempt crowdfunding offerings.

Funding portals are not subject to registration as a broker-dealer, but would be subject to an alternative regulatory regime, subject to SEC and SRO authority, to be determined by rulemaking by the SEC and SRO.

Crowdfunding Proposal

The SEC's proposed rules have proven controversial

Crowdfunding proponents believe that the proposal is too burdensome and would make it challenging for start-ups

Process requirements are too prescriptive and cumbersome

Disclosure requirements for the initial offer (Form C) and ongoing reporting requirements (Form C-A, Form C-U, Form C-AR) would make the process to expensive

By contrast, the SEC's Investor Advisory Committee has recommended stronger consumer protection provisions

In the Meantime...

The SEC staff issued various C&DIs regarding intrastate crowdfunding

Various states have adopted their own crowdfunding exemptions

The proposed full text of the JOBS Act and its amendments may be accessed here.

The Official Bill Summary of the JOBS Act from The Library of Congress may be accessed here.

The Status of the JOBS Act

Since the JOBS Act was signed into law, what is the status of Title II and Title III elements: 8,28

Title II went into effect September 23, 2013, one and a half years after President Obama's signature on the bill

Over two years since approval, Title III has not been finalized and enacted.

Most of the JOBS Act's provisions are not effective until the U.S. Securities and Exchange Commission ("SEC") implementing rules become effective. The SEC has missed all statutory deadlines for issuing rules. The important rulemaking allowing general advertising in private offerings in which securities are sold only to accredited investors finally will become effective on September 23, 2013. The SEC appears to be intent on thwarting Congress's idea of a simple private offering." 8

How soon for Title III?

"Title III would provide a means for nonaccredited investors to begin investing in these companies. It is in process but not likely to be implemented any time soon. The restrictions proposed by the SEC, including additional costs for compliance and heightened liability, would probably not appeal to the best startups that are better served raising capital from accredited investors."

Ryan Caldbeck, "Happy Second Anniversary JOBS Act", April 2014. Forbes.com. 27

Title II Compared to Title III

A brief summary of some key aspects of Title II vs. Title III regulations from Startup Law Blog: 32

Table 2. Title I vs. Title II

Title II [Rule 506(c)]

Title III (Crowdfunding)

Legal Yet?

Yes

No

Individual Investor Limits?

No

Yes

Aggregate Fund Raise Cap?

No

Yes: $1 million in one year

Advertising Allowed?

Yes. Companies can use any type of media they like.

No, once legal, issuers will not be able to "advertise the terms of the offering, except for notices which direct investors to the funding portal or broker."

Eligible Investors?

Only accredited investors

Both accredited and nonaccredited investors can participate.

Broker or Intermediary Required?

No

Yes

Mark Roderick, an attorney at Flaster/Greenberg, has developed what he calls "A cheat sheet on crowdfunding". It is provided below and provides a succinct and practical overview of the area.

Mark Roderick's crowdfunding cheat sheet as of June '14.

Crowdfunding Cheat Sheet

Title II - Rule 506(c)

Title III

Title IV - Regulation A+

Existing Regulation A

Rule 504

In Effect Today

Yes - since 09/23/2013

No - Regulations have been proposed but not yet finalized

No - Regulations have been proposed but not yet finalized

Yes

Yes

Maximum Dollars Raised

No maximum

$1 million per 12 months

$50 million per 12 months

$5 million per 12 months

$1 million per 12 months

Permitted Investors

Only Accredited

Anyone

Anyone

Anyone

Anyone

Per-Investor Limits

None

Yes - depends on income and net worth of investor

Yes - 10% of income or net worth, whichever is more

None

None

General Solicitation Permitted

Yes

Yes

Yes

Yes

Yes

Exempt from State Registration

Yes

Yes

Yes

No

No

Sold Through Portals

Yes

Yes

Not explicitly

No

No

Portals Required to Register

No, provided activities are limited

Yes

Only licensed broker/dealers

Not applicable

Not applicable

Portals Allowed to Pick and Choose

Yes

No

Not applicable

Not applicable

Not applicable

Pre-Sale Information Required

None

Substantial

Very substantial, akin to a mini-registration statement for a public company

Very substantial, akin to a mini- registration statement for a public company

None

Audited Financial Statements Required

No

Sometimes - depends on size of offering

Yes

No

No

Pre-Sale Approval Required

No

No

Yes - submission must be approved by SEC

Yes - submission must be approved by SEC

No for Federal purposes

Available to Foreign Issuers

Yes

No

Only Canada

Only Canada

Yes

Available for Sale of Owner Shares

No

No

Yes

Yes

No

Subject to "Bad Actor" Disqualification

Yes

Yes

Yes

Yes

No

Ongoing Reporting

None

Moderate

Substantial ongoing reporting, akin to a mini-public company, but waived depending on number of investors

None

None

Mark Roderick is an attorney at Flaster/Greenberg PC concentrating his practice on the representation of entrepreneurs and their businesses. He maintains a Crowdfunding blog, which he believes contains news, updates, and links to important information pertaining to the JOBS Act and how Crowdfunding may affect your business. For more information from Mark, email him at mark.roderick@flastergreenberg.com, or follow him on twitter@CrowdfundAttny, or visit his blog at www.crowdfundattny.com.

What is an Accredited Investor?

The JOBS Act states that only accredited investors are eligible to participate in Title II funding. The definition of an accredited investor from the U.S. Securities and Exchange Commission (SEC): 5

a bank, insurance company, registered investment company, business development company, or small business investment company;

an employee benefit plan, within the meaning of the Employee Retirement Income Security Act, if a bank, insurance company, or registered investment adviser makes the investment decisions, or if the plan has total assets in excess of $5 million;

a charitable organization, corporation, or partnership with assets exceeding $5 million;

a director, executive officer, or general partner of the company selling the securities;

a business in which all the equity owners are accredited investors;

a natural person who has individual net worth, or joint net worth with the person's spouse, that exceeds $1 million at the time of the purchase, excluding the value of the primary residence of such person;

a natural person with income exceeding $200,000 in each of the two most recent years or joint income with a spouse exceeding $300,000 for those years and a reasonable expectation of the same income level in the current year; or

a trust with assets in excess of $5 million, not formed to acquire the securities offered, whose purchases a sophisticated person makes.

InvestGeorgia.org has estimated that there are between 3.3 and 8.5 million accredited households in the U.S. [FYI: Georgia and Kansas are two states that have launched their own equity crowdfunding rules]. 34

The Developing World and Crowdfunding

"Crowdfunding's Potential for the Developing World", a 2013 report published by the World Bank, focused on crowdfunding in the developing world. Given the rather immature nature of crowdfunding in most countries, what the report stated regarding crowdfunding has relevance in nearly all countries, not just the developing world: 13

"The closed and private nature of investing in small businesses and start-ups will change rapidly as the social web affects the flow of both information and capital to these companies."

"The rise of crowdfunding as a more distributed way to form capital is aligned with the changes in the flow and distribution of information (via the Internet) and the creation and distribution of manufacturing capabilities (maker spaces and fabrication centers)."

"Existing securities regulations were not crafted for the social web. Governments and policy experts worldwide are considering the possible impact of crowdfunding and crowdfund investing and trying to fashion new regulations, empower new technologies, and equip entrepreneurs with sufficient information to decide if crowdfunding is a viable funding or investment vehicle for these enterprises."

"The rate of growth of crowdfunding, and its emergence in developing and developed countries, suggests that this phenomenon can become a tool in the innovation ecosystems of most countries."

The third point, related to laws and regulations, has naturally the greatest potential impact. In the US, Title II is legal and operable, while Title III is not yet approved and its revision and approval process continues.

What is the Future of Crowdfunding for Life Sciences?

For the start-ups and other life science companies needing funding, Title III crowdfunding can only provide up to $1 million per year. Though not insignificant, most companies in this space will quickly evolve to need much higher amounts to continue development (entering the Valley of Death phase). This is where the promise of Title II "Crowdfunding" shines brightest. Title II is solely related to general solicitation rules, but the mere act of removing those prohibitions allows using the internet to advertise solicitations, i.e., by definition, crowdfunding. This is where the accredited investors sitting on the sidelines (remember, it is estimated that only 3% of accredited investors are active) can now more easily participate in investing. Internet-based Title II funding portals will enable those 97% of accredited investors, who may not be well-connected and/or located in areas of high VC activity (Silicon Valley, etc...), to have access to review and participate in funding life science opportunities with ease.

Promising: Title II & Crowdfunding

Internet-based Title II funding portals will enable those 97% of accredited investors, who may not be well-connected and/or located in areas of high VC activity (Silicon Valley, etc...), to have access to review and participate in funding life science opportunities with ease.

For life sciences to continue to attract future investments, success will hinge on the value proposition of the investment opportunity. Though crowdfunding methods will make investing easier and more accessible, future life science opportunities must continue to offer more significant potential value than other category opportunities. After all, for most investors, the return on investment is the force driving their investing.

Additional Reading & Information Sources

Additional reading and sources of information; provided in no particular order: